From damaging floods to burst pipes, water damage is one of the most common personal insurance risks. Just one inch of water can cause $25,000 in damage to your home.[1] According to one insurer, non-weather-related water losses are the number one source of property damage.[2] Among our own clients — large families and family offices specifically, who often have secondary homes — non-weather related water losses are the most common, accounting for approximately one-third of all homeowners claims over a ten-year period.[3]

Does homeowners insurance cover flood damage?

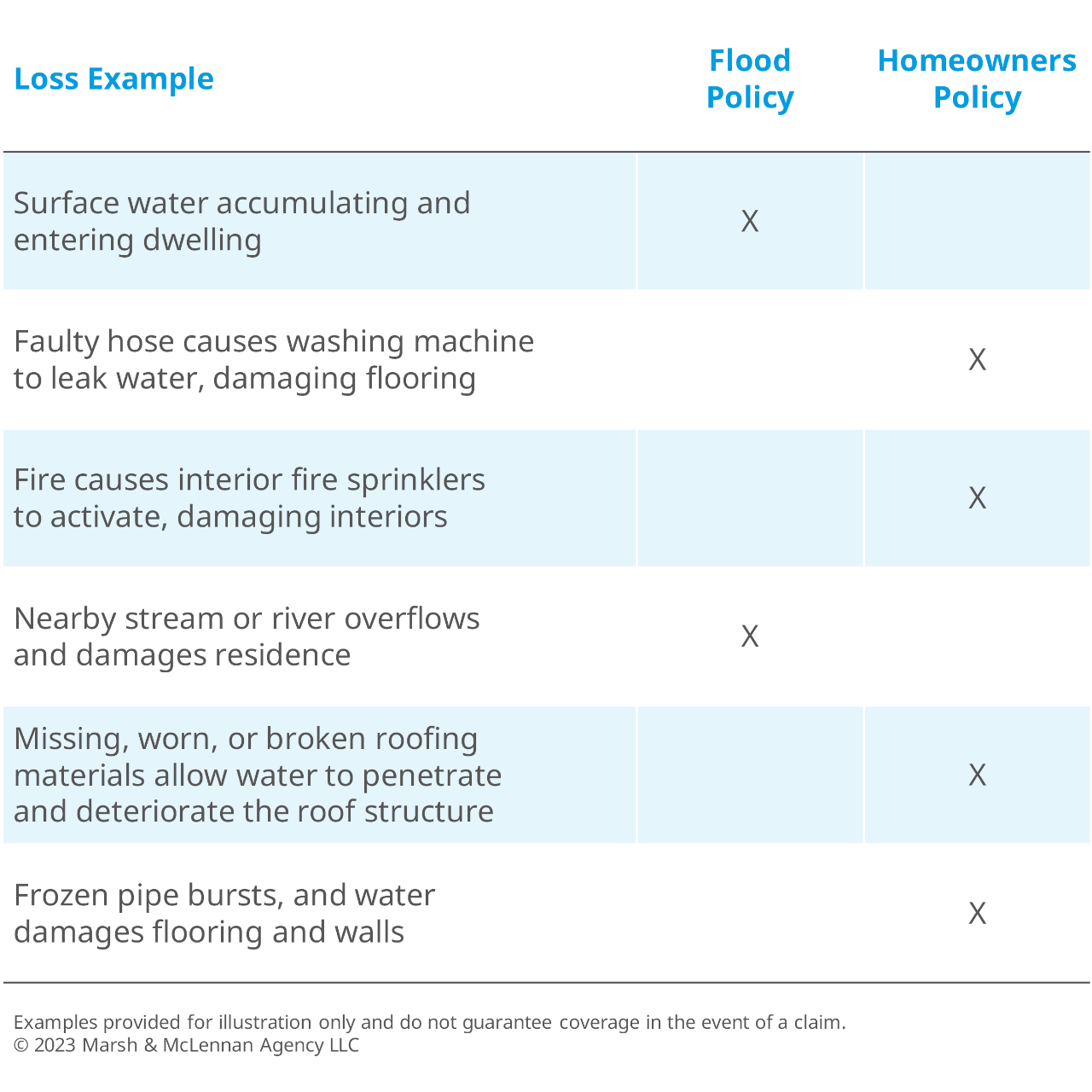

Because damage caused by flooding is not covered by most homeowners policies, as homeowners, it is important to understand the difference between a flood loss and other types of water damage.

Water damage can come from many different sources – a broken pipe, a hole in a damaged roof, or a water backup.

In general terms, flooding is usually caused by rising water from outside the home. Insurance advisors often hear a common misconception, “my home isn’t in a flood zone; I don’t need flood insurance.” Every home is in a flood zone, but homes in lower risk zones are typically not required to carry flood insurance by mortgage companies. Homes in high-risk areas have a 26 percent chance of suffering a flood over the course of a 30 year-mortgage, as reported by FEMA. In fact, homes in high-risk areas are 2.5 times more likely to suffer a flood than a fire.

So, is it flood damage or is it water damage? The information below outlines which policy may respond to a given scenario: