Erika Almquist

Palm Beach Gardens, FL

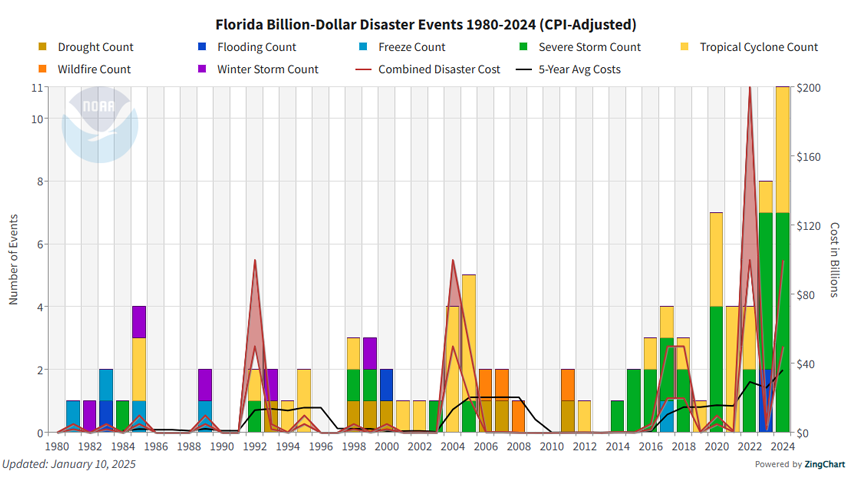

The allure of warm winters, mild seasonal changes, and the “endless summer” lifestyle has helped Florida’s population surpass 23 million, a gain of 1,476,364 residents (6.9%) since the 2020 Census. As Florida's population continues to grow, the threat of catastrophic flood and wind damage from increasingly powerful hurricanes casts a shadow over millions of residents, making preparedness more crucial than ever.

In 2024, Hurricane Milton caused an estimated $21 billion to $34 billion in insured and uninsured damages, and that was on the heels of Hurricane Helene, which affected a total of 16 states and caused an estimated $30.5 billion to $47.5 billion in total insured and uninsured wind, inland flood, and storm surge damage. Together, these two storms generated over 80,000 National Flood Insurance Program (NFIP) claims, with projected losses of an estimated $7.5 billion to $9.5 billion in flood claims alone according to Neptune Flood’s report.

While hurricanes have become more frequent and severe in recent years, the threat of damage from catastrophic weather events is not the only factor driving a decrease in capacity and increased insurance costs in the state. Increased legislation has increased the cost of claims. The Florida Office of Insurance Regulation reports that Florida accounts for only 9% of the nation’s homeowners’ claims but 79% of homeowners insurance lawsuits. The Florida Office of Insurance Regulation states that over a 10-year period, 71% of the $51 billion paid by Florida insurers went to attorneys’ fees and public adjusters. In total, these parties have received more claims settlement money than policyholders. In 2023, the industry posted collective underwriting losses of $190.8 million, marking the eighth straight year of losses, according to S&P Global. As a result, insurance in Florida continues to be scarcer and more expensive.

With the potential for increased tropical storm activity and the mounting cost of claims in the state, the Florida homeowner’s insurance market continues to be in what is known as a “hard” market. When an insurance market turns hard, it means increases in price and decreases in product availability, both of which make it harder for homeowners to find the coverage they need.

A hard insurance market is a reminder that insurance is based on the law of large numbers. When losses increase by frequency, severity, or both, then the overall pool of premium must increase to offset those losses. The simple fact that a policyholder was not directly impacted by a recent storm or other loss event does not solely determine the impact to their premium or insurability. For example, in Florida, the year a property was built, its location, and its wind mitigation features are the biggest factors driving rates and insurability. So, while those with a higher risk profile will see the greatest impact, all homeowners in the state are still affected.

In 2024, many Florida homeowners are receiving non-renewal notices, and others are facing unprecedented rate increases. Insurance companies are looking to reduce their exposure to losses in the state and are passing on their increased costs to the consumer. As a result, a significant amount of Excess and Surplus (E&S) business is being written in Florida. E&S insurance provides coverage for unique or high-risk situations that standard insurers may not cover, allowing for more tailored policies. Additionally, the surplus lines market is becoming increasingly important as it offers specialized products for risks that traditional insurers are unwilling to underwrite.

Further, the ability to obtain new or replacement coverage has become increasingly difficult, with many insurers implementing extremely strict new business guidelines. For example, policies may cost significantly more to obtain, may exclude wind coverage, or include an extremely high wind deductible. Rate and policy changes like these can be challenging to understand, so let’s take a more detailed look at some of the contributing factors.

Many people are surprised to learn that the amount they should insure their home for is based on how much it would cost to rebuild the home, rather than the market value. In Florida, reconstruction costs increased between 4.2% and 5.1% from October 2023 to October 2024, largely because of supply chain disturbances with materials and labor issues. After a hurricane, there is often a local shortage of materials and skilled labor, which impacts reconstruction costs and the time it takes to repair or rebuild a home. These factors all result in higher premiums for both new and renewal policies.

In addition, if you are not able to reside in your home due to a covered loss, the cost to rent a similar home is often much higher in Florida than in other states. The high demand for rental properties during the season drives up the additional living expense portion of the loss, resulting in higher claim payments.

Because of the severity of the loss potential, a separate deductible typically ranging from 2% to 15% of the insured value of the home applies to hurricane-related claims. Notably, many carriers have increased their minimum allowable hurricane deductible from 2% to 5% of the dwelling limit of the home. Policyholders should be aware that the hurricane deductible in Florida is per calendar year rather than per incident. Thus, it is important to report all hurricane claims, even if the loss is below the deductible, as there may be multiple storms during the year. Often, the policy terms include a condition that shutters or other hurricane protection must be in place on the property during a named storm.

For details and hurricane mitigation strategies, read our Homeowner Risk Mitigation Insights article.

The threat of damage caused by flooding also increases with hurricanes. Storm surge is a threat for properties near the coast, but inland properties can also face the risk of flooding due to considerable amounts of rainfall they experience in the aftermath, as was the case in Hurricane Ian. Homeowners’ policies do not typically include coverage for flood, and separate coverage should be secured before a pending storm, as there is up to a 30-day waiting period for flood insurance.

Flooding is a big concern in Florida, especially given the recent events of Hurricane Helene and Milton. During those hurricanes, many homes not elevated above Base Flood Elevation (BFE)—the expected elevation floodwaters are expected to reach during storms—sustained damage. Florida homeowners with below-BFE properties can work with specialized companies to lift their homes to a higher and safer level.

For details and flood mitigation strategies, read our Rising Waters blog.

Insurance companies in the state of Florida have also increased premiums due to fraud and higher claims payments related to the assignment of benefits (AOB) clause. This clause in Florida homeowners’ policies allows a homeowner to assign the right to receive insurance proceeds to a third party. Unfortunately, in the recent past, unscrupulous contractors have been submitting inflated claims to insurance companies and then filing lawsuits under a Florida law that guarantees payment of their legal fees if they prevailed. The carrier would adjust the claim, offering a lower settlement to reflect true costs, only to be served with a lawsuit. Despite recent law changes to this clause, data from the OIR and the DFS' Service of Process database show continued abuses.

In 2022, Florida Governor Ron DeSantis signed a property insurance reform bill to help stabilize the Florida property insurance market, increase competition, strengthen consumer protections, reduce litigation, and prohibit the use of assignment of benefits for policies issued on or after January 1, 2023. The bill worked as intended in 2023, with the number of lawsuits filed against insurers during the first three quarters declining by 23.8%—from 36,639 to 27,923—compared to the same period last year. The number of lawsuits filed also declined by 30% compared to the third quarter of 2023. This decline could also be attributed to the absence of major hurricanes in Florida in 2023, with the effects of Hurricanes Helene and Milton being watched closely.

It is always a good practice to thoroughly review and understand any contracts with repair companies, as signing an AOB may put the claim settlement at risk.

To avoid overpaying or being underinsured, it is important to have the most complete information available about a property before evaluating coverages and pricing. Having specific reports and documentation is vital to providing the full picture of a home’s risk profile.

One key determining factor is the year that a home was built, as the Florida Building Code (FBC) changed for most of the state, with the exception of Naples, on September 1, 2002. The 2002 building code included enhanced requirements to build stronger homes to protect against wind-related damage. Similarly, the 2008 Florida Building Code further strengthened these requirements by incorporating updated structural design criteria and flood protection measures, significantly improving the resiliency of homes against severe weather events. City and county codes also aim to ensure a home is built to withstand weather events.

If a home has been renovated, it is important to ask for details about the extent of the renovation. In Florida, a home may be taken down to the studs but can keep two original walls standing to maintain the tax status of the property. As a result, some insurance companies will agree to consider the year of the renovation as the year the home was built instead of looking at the year it was originally constructed.

Regardless of when a home was built, it is best practice to ask for a wind mitigation inspection report. While a home built after the FBC change should have all these characteristics, some insurers are looking to confirm these standard requirements:

There are a lot of great wind-rated products on the marketplace that hold up longer than traditional products like asphalt shingles. If you are considering replacing your roof, reach out to the risk advisory team at MMA to discuss potential considerations, including:

Buyers should ask for a four-point inspection on a home built prior to 2002. This inspection report will note the age of the home’s systems, such as electrical panels and the roof. A roof older than 15 years will impact the home's insurability, even though certain roof covering materials have a useful life of 25 to 30 years.

Homeowners’ policies do not include coverage for damage resulting from floods, and buyers should speak to their insurance advisor regarding purchasing flood insurance. The seller is required to disclose if they have filed a claim related to flood damage on the property and if they received federal assistance for flood damage to the property. Buyers should also ask for an elevation certificate if the home is in a high-risk flood zone (Zone A or V). Most insurance companies need to confirm the home is positively elevated to be eligible for coverage. Homes built prior to 1970 might not be positively elevated, and this will impact your premium. Flood, wind, and hurricane protection program coverages are all important considerations, regardless of the flood zone of the property.

All these reports are in addition to the standard home inspection typically performed as part of the real estate transaction process. Some of this information may still be required even if the homeowner wants to self-insure for wind coverage, such as renovation information, a wind mitigation inspection report, a four-point inspection, and an elevation certificate.

Additionally, when there is a mortgage, it is important for the buyer to confirm that it will be insurable at a reasonable cost before making an offer or finalizing the closing. Just because a property is currently insured by the seller does not guarantee the home will continue to be insurable in current market conditions. Likewise, if you are planning to sell your home, a prospective buyer may want to make sure coverage can be obtained on the property before making an offer or closing.

If you are selling your Florida home, having the reports mentioned previously on hand for the potential buyer will help the transaction move along more smoothly.

Despite this challenging time of change in the insurance marketplace, there are some steps current homeowners can take to help maintain their insurability, no matter where they live. Homeowners can:

If you haven’t completed a comprehensive review of your personal insurance recently, now is a good time to schedule one with your insurance advisor.

Clients faced with the challenges of a hard market often benefit from the expertise provided by a professional insurance advisor who works with multiple insurance companies and can provide counsel and advocacy. Whether you are buying a new home, looking for new coverage after a non-renewal, or considering changing insurers after a steep premium increase, we are happy to assist you in navigating your insurance options.

Schedule an insurance review with a personal risk advisor to learn more about the liability exposures related to the Florida market and ensure you have the proper insurance protection.

Palm Beach Gardens, FL

Naples, FL

Tampa, FL