Bill Sautter

Financial Well-being Coach

Retirement planning has undergone significant transformations over the past few decades, with the introduction and evolution of 401(k) plans playing a pivotal role. Americans currently hold approximately $7.8 trillion in 401(k) plans, according to the Investment Company Institute.

As employees continue to seek the best ways to secure their financial future, understanding the history and differences between Roth and traditional 401(k)s has become increasingly important. In this article, we will explore the evolution of 401(k) plans and delve into the key distinctions between Roth and traditional contributions to help you make informed decisions about your retirement savings.

The great debate between 401(k)s and Roth IRAs was not much of a debate less than 30 years ago. For decades, traditional contributions, or pre-tax dollars, were the one and only way to contribute to a Section 401(k) plan.

In the mid-1970s, there was important litigation taking place in Congress, and laws were passed that would change the United States retirement system as we know it: the Employee Retirement Income Security Act (ERISA). This piece of legislation laid the groundwork for employer 401(k) plans and individual retirement accounts (IRAs). Before ERISA, cash or deferred arrangements (CODAs) were used to fund pension plans, stock bonuses, and profit-sharing plans.

Four years after the ERISA Act was passed, the Revenue Act of 1978 paved the way for the modern 401(k) plan as we know it. This act included a provision in the tax code allowing employees to defer compensation from bonuses or stock options into a retirement savings plan. Although there are still pension plans out there today—mostly in the public sector—many of these plans are rare due to employer liability and the popularity of the 401(k) plan.

During the 1980s and 1990s, the popularity of 401(k)s surged as companies began to shift from defined benefit plans to defined contribution plans. This shift was driven by the rising costs and financial risks associated with maintaining pension plans. Employers favored 401(k) plans because they transferred the investment risk to employees and provided predictable costs through employer matching contributions.

Over 20 years later, a group of legislators, led by Senator William Roth (R-Del.), passed the Taxpayer Relief Act of 1997, which introduced the Roth IRA. Almost 10 years later, in 2006, the Roth 401(k) made its way into the retirement investing community. This provided hardworking Americans with choices that were not available to them before.

Let’s look at historical tax rates in the U.S. and around the world for insight into where global and domestic tax rates are shifting as a result of a trend in globalization movements and organizations.

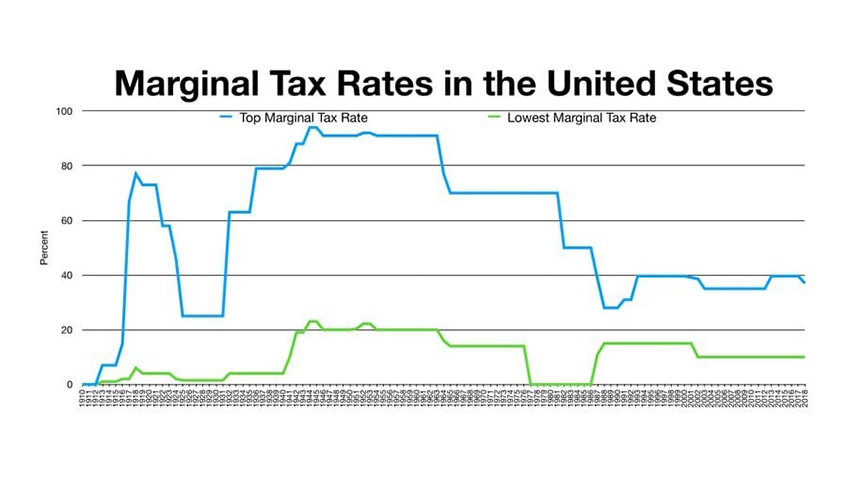

Looking at historical U.S. marginal tax rates, we can see that in the early 1940s, during World War II, rates reached above 90%. Back then, 401(k) plans, let alone Roth options, didn't exist, leaving no room for debate. Paying taxes upfront would have been seen as a poor decision, as it would result in most of your hard-earned income going directly to the federal government.

Now, however, tax rates have declined for several reasons: to spark economic activity, personal consumption, increase individual savings, and more. More recently, we see that, besides the 1%, the other marginal tax brackets have been declining due to the Tax Cuts and Jobs Act passed in 2017, which has temporarily lowered marginal tax rates and widened tax brackets. The U.S. is experiencing some of the lowest tax rates going back almost 100 years. Now may be a time to take advantage of the historically low rates and make Roth contributions to protect yourself from the downside of increasing tax rates, like we saw in the middle of the 20th century.

Source: Graphic Credit: Guest2625, CC BY-SA 3.0 <https://creativecommons.org/licenses/by-sa/3.0>, via Wikimedia Commons

Source: Graphic Credit: Guest2625, CC BY-SA 3.0 <https://creativecommons.org/licenses/by-sa/3.0>, via Wikimedia Commons

If U.S. taxes are bottoming out after a steady decline over 60-plus years and do end up rising from here, the logical decision would be to make Roth contributions, depending on your personal situation in retirement. On the other hand, if tax cuts remain a prevailing trend, pre-tax contributions might be more advantageous.

Ultimately, the best approach will depend on your individual financial situation and retirement goals, making it crucial to evaluate your options carefully and seek professional advice to maximize your retirement savings strategy.

For more information on 401(k) plans and to gain a deeper understanding of your retirement options, don't hesitate to reach out to your MMA Prosper Wise℠ team. Our knowledgeable advisors can provide personalized guidance tailored to your financial goals, helping you navigate the complexities of retirement planning and identify the most suitable strategies for securing your future. MMA Prosper Wise provides tools, education, and personalized coaching to help you prepare for and manage your retirement plans. Learn more about our retirement tools and resources.

Securities and investment advisory services offered through MMA Securities LLC (MMA Securities), member FINRA / SIPC, and a federally registered investment advisor. Main Office: 1166 Avenue of the Americas, New York, NY 10036. Phone: (212) 345-5000. Variable insurance products distributed by MMA Securities LLC, CA OK 81142. Marsh & McLennan Insurance Agency LLC and MMA Securities LLC are affiliates owned by Marsh & McLennan Companies. Investment advisory services for MMA Prosper Wise℠ are offered solely as a Registered Investment Adviser through MMA Securities. Certain of our investment adviser representatives are registered representatives of MMA Securities. A copy of our written disclosure statement discussing our advisory services and fees is available for your review upon request. Please consult a tax professional for specific tax inquiries and recommendations. MMARetirement.com

Financial Well-being Coach